Read More

Guest Author: Graham Day, CFA, Chief Investment Officer, Innovator ETFs

Amid record stock market highs but persistent volatility, many investors want equity exposure – just not if it means taking any risk. This is evidenced by the massive amount of cash on the sidelines, with the asset class now making up almost 35% of affluent investors’ portfolios per the Capgemini Top Trends 2024 report. Recent estimates from the Investment Company Institute (ICI) suggest there is more than $6 trillion sitting in money market funds alone.

With high yield savings accounts and money market funds paying 4-5% interest, the fear of loss combined with easy access to a safe option offering a decent rate of return can make cash a compelling proposition. However, the vast majority of money in savings accounts isn’t even earning 4-5%. In fact, as of February 2024, the average money market account rate is just 0.66% according to the FDIC.

Bonds, typically a predictable “safe haven,” can no longer be relied upon for the benefits they have historically delivered, thanks to volatility, rate risk, and credit risk.

So where can investors turn when they are seeking higher yields but still looking for a measure of protection? Increasingly, it’s to the annuities market. In 2023, the annuity sales reached $360 billion, with a record year for principally protected indexed annuity sales at $96 billion per LIMRA.

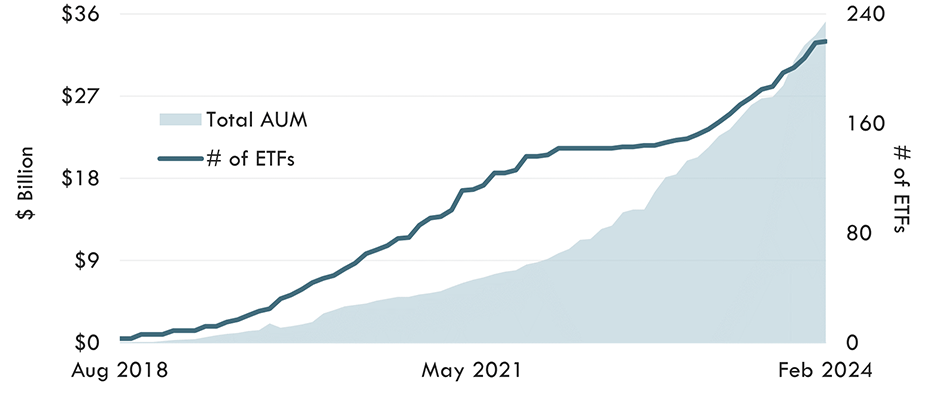

Investors’ appetite for known outcomes has also shown itself through the success of Buffer ETFs, which use options to provide a known level of protection against loss along with equity upside potential, to a cap. Introduced in 2018, the broader category of Defined Outcome ETFs now includes over 200 funds, with more than $35 billion in AUM, including $10 billion in 2023 net flows.

Source: Bloomberg, from 7/31/2018 to 2/29/2024

The latest innovation in the category, known as Defined Protection ETFs, are designed to offer a 100% buffer against losses with capped upside exposure over a two-year outcome period. All of the typical benefits of buffer products – ease of access, no credit risk, tax efficiency, and upside participation with built-in risk management – become magnified in the case of the 100% buffer. Inaugural funds in the category, with upside caps in the range of 16-17%, have amassed hundreds of millions of dollars in flows.

Clearly there is a market for downside protection, but why reinvent the wheel with ETFs when traditional indexed annuities and structured products are ample and thriving?

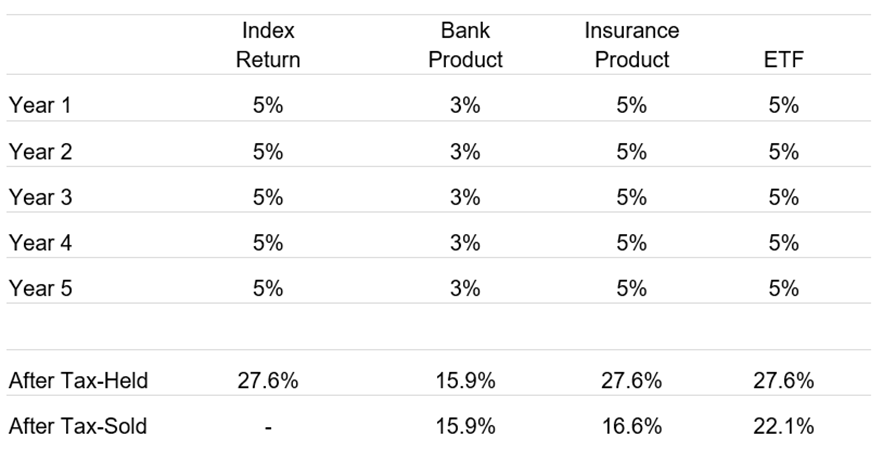

All else equal, higher upside potential for starters, due in large part to the high costs, hidden fees, and illiquidity associated with annuities. But one of the biggest considerations here is tax treatment.

Despite their two-year or longer tenure, structured notes see phantom gains taxed annually as ordinary income. While the taxes on income from a qualified annuity may be deferred for the life of the product, they too are owed at the ordinary income rate.

Meanwhile, the two-year outcome period structure of Defined Protection ETFs means that any gains are given more favorable long-term capital gains tax treatment if held for more than a year and a day.

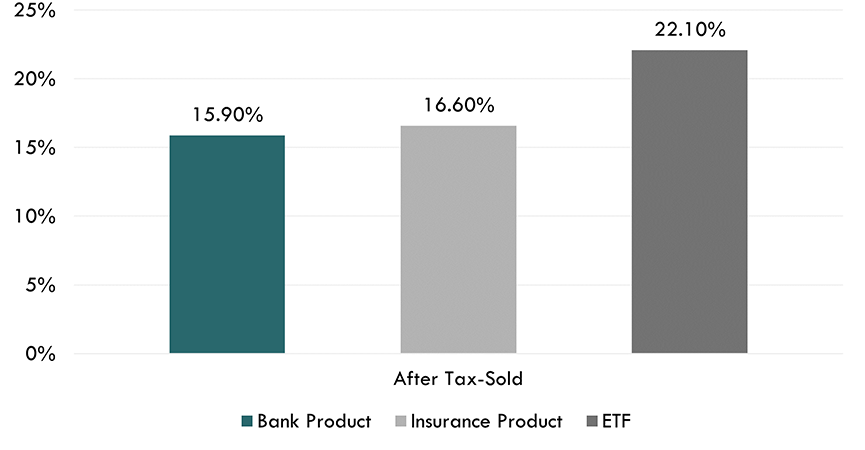

Both in the short term and over an investor’s longer time horizon, these differing tax obligations can add up, giving the ETFs a significant edge and tremendous potential value. As demonstrated by the chart below, an equal investment in each of the aforementioned vehicles could be worth a vastly different amount at the end of a five-year period.

For Illustrative Purposes Only. Does Not Represent Actual Returns.

For illustrative purposes only. Assumes a 40% ordinary income tax rate and a 20% long-term capital gains tax rate.

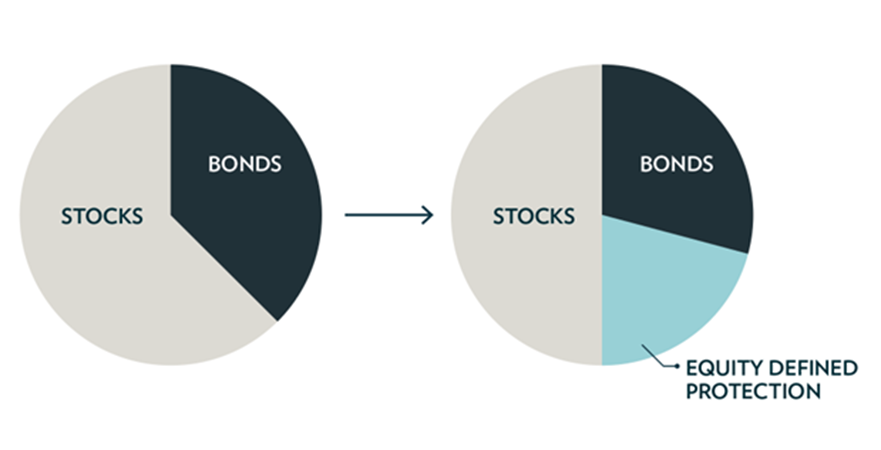

We know that equity market uncertainty and bond market volatility can wreak havoc on investment portfolios. Diversification has always been the name of the game.

While Defined Protection ETFs offer U.S. Equity upside to a relatively large cap, they aren’t intended as a core equity position (though a very conservative equity investor might find them an attractive option for a larger share of their portfolio). Rather, we believe 100% buffer products can supplement a portion of both the equity and fixed income allocation, depending upon the investor’s goals.

The other natural use case involves all of that aforementioned cash that’s waiting in the wings. We speak to advisors regularly who are looking for vehicles to help their more skittish clients get back into an equity position while allaying fears about loss of principal.

The reality is that people are in cash because they want certainty; a bank-insured 4% return may sound more appealing than the chance of a larger gain. But certainty is woven into the fabric of Defined Protection products: the 100% downside buffer and upside cap are known to the investor at the start of the outcome period.

We’re all keeping an eye on forthcoming Federal Open Market Committee (FOMC) minutes and Jerome Powell’s interviews for clues about the trajectory and timing for interest rate moves. At this point, the market is pricing in multiple cuts throughout 2024, and it feels like more of a question of when than if.

When the inevitable cuts occur, cash will become less appealing. This creates a natural opportunity for low-risk products with higher return potential, like Buffer ETFs.

As another feather in the cap for equity market participation, it’s worth noting some important historical context (which, of course, does not guarantee future performance). Over any given two-year period in the history of the S&P 500, there has been a positive return 88% percent of the time.[1]

That said, the excitement over AI that is propping up the market won’t necessarily last forever, and we’re keeping an eye out for the inevitable market sell-off. While investors are already scared and overweight cash, a market dip will further accelerate that retreat. Defined Outcome and particularly Defined Protection strategies offer a way for investors to stay invested, very defensively. And when volatility is high, the upside caps on new series of these products increase, offering an even more compelling proposition versus cash.

[1] Source: Bloomberg, 1950-2023

Given the proliferation of annuities and structured notes – and the piles of cash on the sidelines – there is no doubt about the risk aversion that is shaping today’s portfolios. We see the innovation of Defined Protection vehicles as changing the equation for those who are missing out on key gains but who need some reassurance about the preservation of their assets.

--------------

Tax Alpha is a measure of an investment’s outperformance attributable to tax efficiency. Structured notes are issued as a bank obligation, designed to offer an index-related return. The S&P 500 is a measure of the returns of the common stock of U.S. large-cap companies.

ETFs use creation units, which allow for the purchase and sale of assets in the fund collectively. Consequently, ETFs usually generate fewer capital gain distributions overall, which can make them somewhat more tax-efficient than mutual funds. Defined Outcome ETFs are not backed by the faith and credit of an issuing institution, so they are not exposed to credit risk.

The Fund has characteristics unlike many other traditional investment products and may not be suitable for all investors. For more information regarding whether an investment in the Fund is right for you, please see "Investor Suitability" in the prospectus.

The outcomes that the Fund seeks to provide may only be realized if you are holding shares on the first day of the Outcome Period and continue to hold them on the last day of the Outcome Period, approximately two years. There is no guarantee that the Outcomes for an Outcome Period will be realized or that the Fund will achieve its investment objective.

Investing involves risks. Loss of principal is possible. The Funds face numerous market trading risks, including active markets risk, authorized participation concentration risk, buffered loss risk, cap change risk, capped upside return risk, correlation risk, liquidity risk, management risk, market maker risk, market risk, non-diversification risk, operation risk, options risk, trading issues risk, upside participation risk and valuation risk. For a detailed list of fund risks see the prospectus.

FLEX Options Risk: The Fund will utilize FLEX Options issued and guaranteed for settlement by the Options Clearing Corporation (OCC). In the unlikely event that the OCC becomes insolvent or is otherwise unable to meet its settlement obligations, the Fund could suffer significant losses. Additionally, FLEX Options may be less liquid than standard options. In a less liquid market for the FLEX Options, the Fund may have difficulty closing out certain FLEX Options positions at desired times and prices. The values of FLEX Options do not increase or decrease at the same rate as the reference asset and may vary due to factors other than the price of reference asset.

Graham joined Innovator Capital Management in 2017 and is Senior Vice President, Chief Investment Officer, responsible for product development, capital markets and research efforts. Prior to joining Innovator, Graham was SVP - head of product & research at a startup ETF issuer and a Senior Strategist at Invesco PowerShares. He has been quoted in CNBC.com, TheStreet.com, FA magazine, FOX Business and Investopedia.com. Graham is a CFA charter holder, a member of the CFA Society of Chicago and holds a bachelor’s degree from Wheaton College.

Innovator ETFs are distributed by Foreside Fund Services, LLC.

The Fund's investment objectives, risks, charges and expenses should be considered carefully before investing. The prospectus and summary prospectus contain this and other important information, and it may be obtained at innovatoretfs.com. Read it carefully before investing.

This article is part of Cboe’s Guest Author Series, where firms and individuals share their insights, strategies and ideas with the broader Cboe community. Interested in contributing? Email [email protected] or contact your Cboe representative to learn more.

Disclaimer: There are important risks associated with transacting in any of the Cboe Company products or any digital assets discussed here. Before engaging in any transactions in those products or digital assets, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/us_disclaimers/. These products and digital assets are complex and are suitable only for sophisticated market participants. These products involve the risk of loss, which can be substantial and, depending on the type of product, can exceed the amount of money deposited in establishing the position. Market participants should put at risk only funds that they can afford to lose without affecting their lifestyle. The views of any third-party speakers or third-party materials are their own and do not necessarily represent the views of any Cboe Company. That content should not be construed as an endorsement or an indication by Cboe of the value of any non-Cboe financial product or service described.