Global Markets

Tradable Products

Implied volatilities were mixed across asset classes last week as the US government shut down for the first time since 2018. Interest rate volatility declined meaningfully, with the VIXTLT Index falling to a 1-year low while the MOVE Index collapsed to a 3-year low. In contrast, equity volatility gained last week, with the VIX® index increasing 1.4 pts to 16.7%. This is despite realized volatility grinding to a 1-year low of 5.9%. SPX 1M implied-realized spread widened to the 99th percentile high as a result.

Read MoreLink to Report: Macro Volatility Digest

WHAT STANDS OUT:

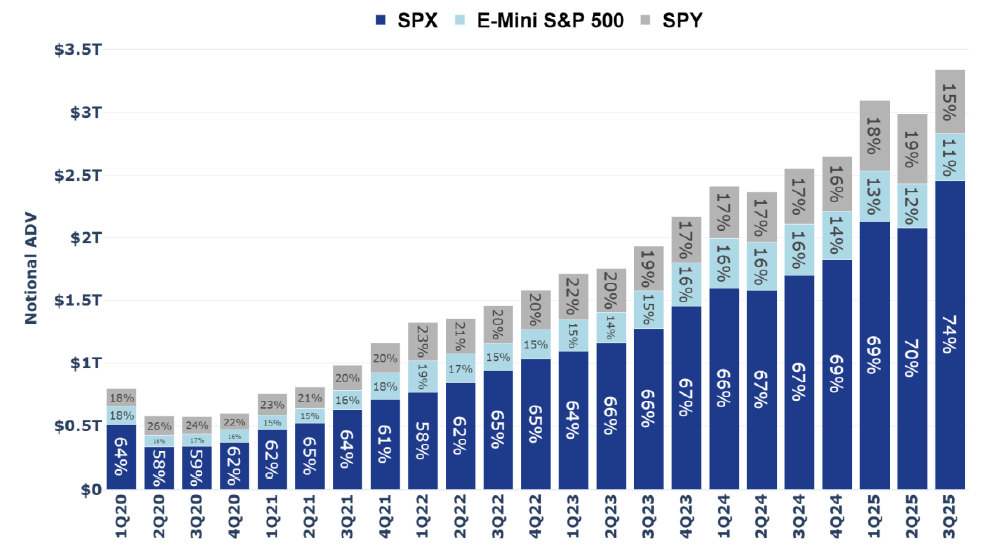

Chart: SPX Options Jump to Record 74% Market Share

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More