Read More

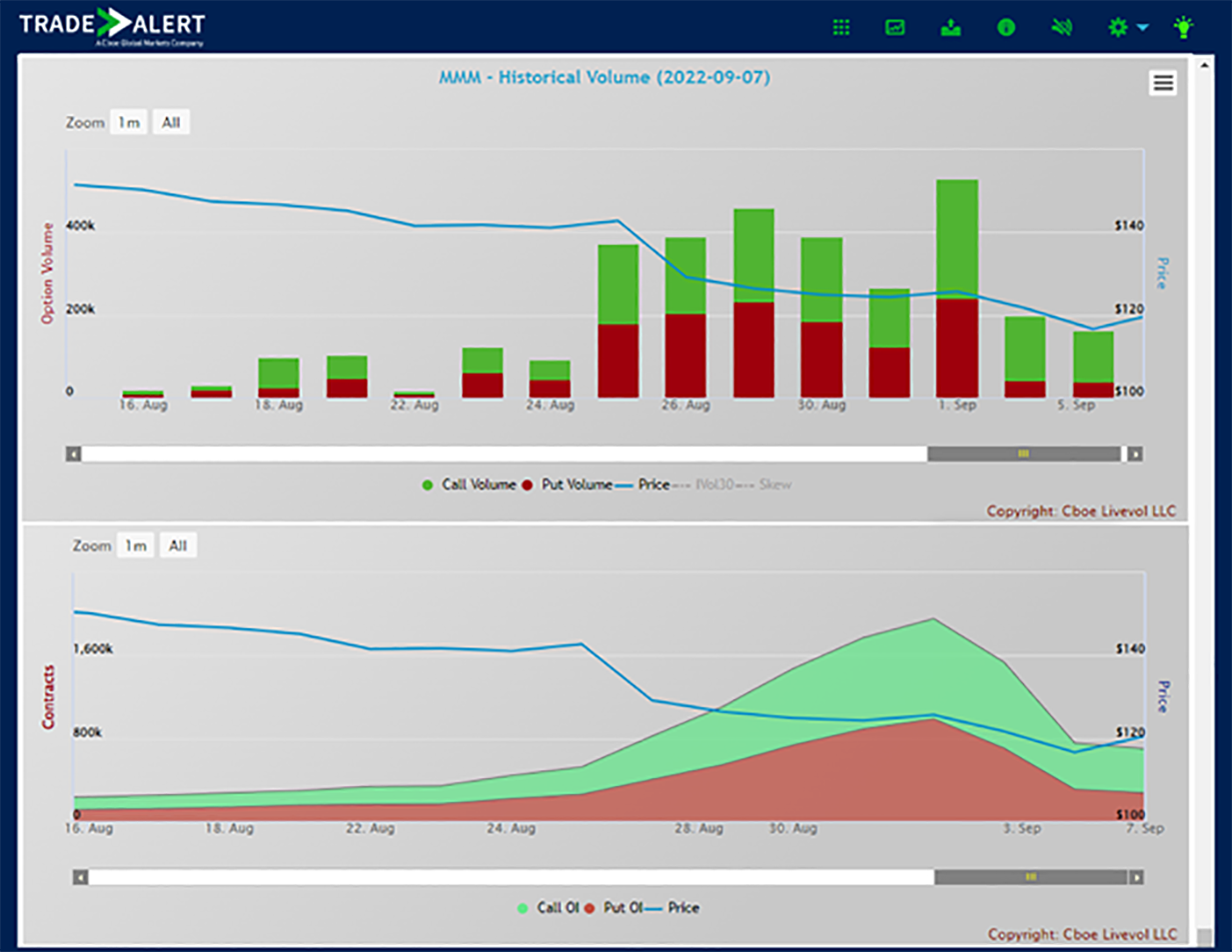

According to Trade Alert data, nearly 3 million option contracts traded in 3M (MMM) between August 25 and September 6, 2022, a level 18 times higher than recent average levels. Additionally, open interest grew by more than 1.4 million to a record 1.95 million contracts. A closer analysis of order flow shows that the unusual volume can be attributed to an arbitrage strategy ahead of 3M’s August 31 tender to spin-off its Food Safety Business and merge it with Neogen (NEOG). Terms of the offer are here.

Source: Cboe Trade Alert

The Trade Alert spread recap for this period is dominated by a number of large 3M reverse/conversion spreads, also known as revcons, which combine a position in a put and a call of the same expiration and strike with a block of underlying stock matching the notional size of the options.

This type of spread trades frequently on stocks and ETFs as a non-directional balance sheet trade, with the market risk of the options combination offset by the stock trade. It’s also a way for stock loan traders to lock in a financing rate for a specific time horizon as the price difference between the put/call combination and spot price is simply a function of interest rates, dividend and borrow costs.

In this case, the 3M revcons were executed for a different purpose: to capture the discount offered to investors tendering 3M stock for shares of the spinoff company. As specified in the terms, 3M was offering $107.53 worth of Neogen stock for each $100 of 3M stock as an incentive to facilitate the transaction. In addition, the exchange rate for 3M to Neogen was based on an average of three days of price history, which ended on August 29 and valued 3M at $133.99 per share — well above the August 31 closing price of $124.35, the final trading day before the tender deadline. As part of the deal, 3M limited the number of shares accepted for tender to 15.7 million, with shares accepted on a pro-rata basis if more shares were tendered than the maximum.

Walking through the mechanics of this trade provides an estimate of economics for the arbitrageurs and the risks they took in the process. For illustration purposes, we will analyze the massive 100,000 lot revcon trade that printed on Monday, August 29.

1. A trader executed a conversion in 3M, buying 10 million shares of stock for $127 per share, selling 100,000 September 2 180 calls for $.25, and buying 100,000 September 2 180 puts for $53.85.

Source: Cboe Trade Alert

This 3-leg spread is executed as a package on the trading floor or via the complex order functionality on an exchange. In practice, the net price is expressed as the difference between the stock price ($127) and the net synthetic — the call price - put price + strike price ($126.40) — which works out to -$.60 in this trade. The actual net dollar outlay before fees is just over $1.8 billion. Using the 180 strike avoids any chance of early exercise by the call buyer, and the market risk of the position is effectively zero.

2. The trader elected to tender all 10 million shares of 3M for Neogen shares at a ratio of 6.7713. This ratio is specified in the deal terms and reflects both the 7.53% discount and the price averaging for each stock. It is important to note that the deal terms limit the number of shares that will be accepted to 15.7 million, so the trader is not expecting all 67,713,000 shares of Neogen, but rather a pro-rata allocation based on the total tendered by all participants.

3. The trader awaited the results of the tender. In this example, if there was no cap on the shares accepted, the trader would expect to receive 67,713,000 shares of Neogen valued at $1.41 billion based on the August 31 $20.90 close and would still own the deep-in-the money 180 strike puts from the conversion, which were valued near $556 million based on the August 31 close of $55.65. The combined holding value is $1.96 billion, which suggests a gain of nearly $160 million, or nearly 9%, on this short duration trade. In practice the proration will cut down the number of spin-off shares received by a significant factor. Listed option open interest is used to help traders estimate the number of shares that will be tendered.

Source: Cboe Trade Alert

As shown in the Trade Alert data, nearly 1.7 million contracts were opened in the high strikes used for the strategy, suggesting 845,000 revcons tied to 84.5 million shares which is more than 5 times the cap specified in the deal, leading to an initial proration estimate of 20%. In addition, institutions often use swaps and over-the counter (OTC) derivatives in a similar manner, suggesting an even lower proration. In this case, 3M reported that 203 million shares were tendered, yielding a final proration of just over 7%. This means for every 100 shares submitted by institutional holders only seven were converted into Neogen. Shareholders submitting below 100 shares received the full conversion.

4. The position may be unwound after the tender is completed and shares of the new spinoff company are allocated and available for trading. While the strategy was initially market neutral, once shares are tendered the trader will have residual positions in both 3M and Neogen, which will need to be liquidated in the market. In the theoretical case, where all 10 million shares were converted to 67.7 million Neogen shares, the trader would need to sell all those shares in the market to monetize the discount.

5. Risks of this strategy come into play primarily after the tender deadline. Based on the final ratios, the strategy captured a discount near 9% based on the August 31 closing prices, but a decline of that magnitude in Neogen before shares are sold would wipe that out and the trade could end up losing money. In addition, the trader may have exposure to the price of the 3M as the options legs of the revcon were sized to match shares before the tender. In practice, most institutional traders pre-position and/or hedge to some extent but individual timing and proration estimates can lead to very different results among traders.

Historical data compiled by Trade Alert indicates revcon spreads have made up nearly 700,000 contracts per day in market volume this year, or about 2.2% of the daily volume, while notional value typically exceeds $3 billion, compared to average levels near 300,000 contracts and $2 billion in 2021. While tender-related revcons provide occasional spikes in activity, the primary drivers remain stock-loan and balance sheet traders taking advantage of better exchange technology for handling complex orders and innovations made by brokers and routing firms.

Source: Cboe Trade Alert

Trade Alert systems specialize in cutting-edge order-flow analysis, adding real-time context and unique insight to market activity for a highly automated and fragmented market. The next time there’s a big market move, be in the know with Trade Alert’s expert commentary, front-end platform, APIs and data services. Learn more.

There are important risks associated with transacting in any of the Cboe Company products or any of the digital assets discussed here. Before engaging in any transactions in those products or digital assets, it is important for market participants to carefully review the disclosures and disclaimers contained at https://www.cboe.com/us_disclaimers/.