Read More

The first outcome-based Exchange Traded Funds (ETFs) introduced in 2018 featured buffer fund mandates comprised of variations on a funded option collar that set a target buffer over an outcome period defined by the strategy’s time to expiration.

Cboe® was well-equipped to support ETFs with these directives as structured products regularly use bespoke option strategies. With the right market structure in place, outcome-based ETFs have flourished alongside their structured note predecessors, bringing to market a diversity of reference assets, buffer ranges and risk mandates in an accessible, transparent wrapper.

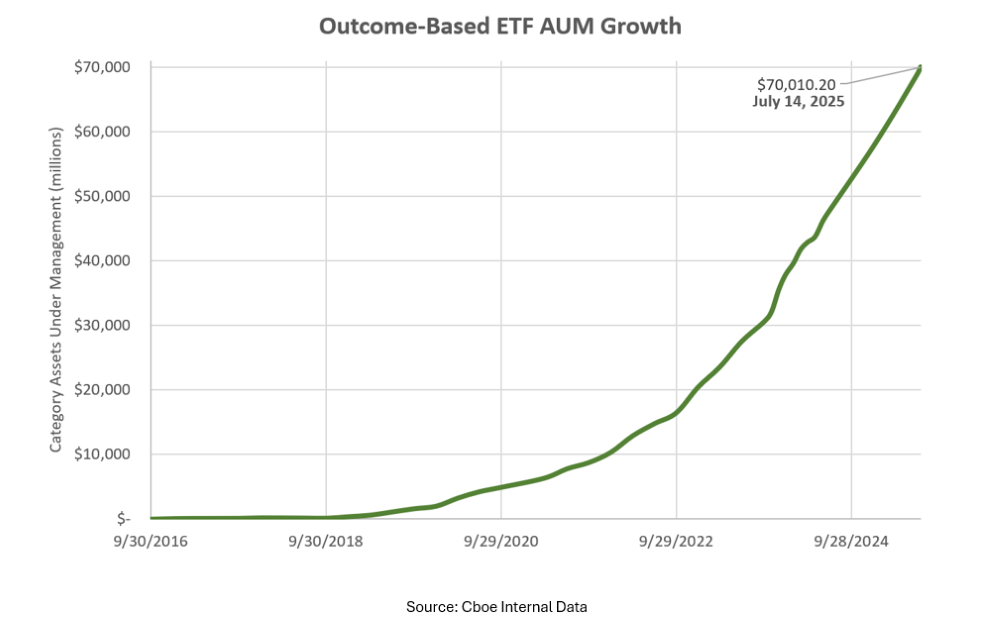

Outcome-based ETFs quietly surpassed $70 billion in assets under management in July 2025, but this milestone may be just the beginning. Strategists continue to set bullish assets under management (AUM) targets1 fueled by an ever-expanding universe of structured product solutions offered by banks, insurance providers and now ETF providers.

Today, 98% of outcome-based ETF assets feature buffer strategies. Over $52 billion is allocated to 9-15% buffers, nearly $13 billion is allocated to 15-40% buffers and just under $3.5 billion is allocated to 100% buffers. The most popular reference asset? ETFs tracking the S&P 500® Index. ETF FLEX® options, in particular, are becoming an increasingly popular tool because of their ability to precisely accommodate structured mandates and their suitability for the ETF primary market.

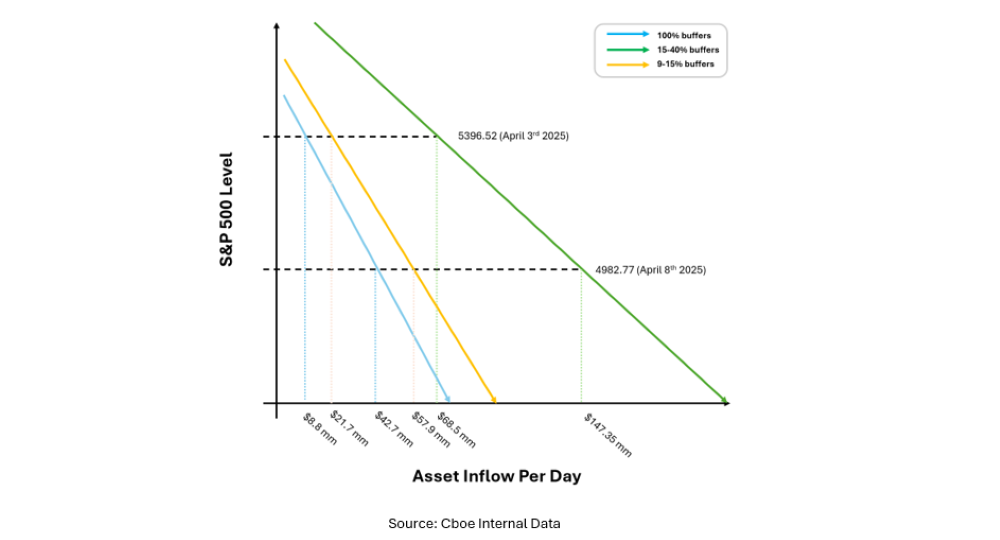

Following market coverage of the early April 2025 tariff announcements, Cboe’s ETP Market Intelligence team analyzed buffer ETF flows2 and observed dynamic reallocation of investor assets from the bellwether 9-15% buffer category into the deeper 15-40% buffer category while S&P 500 Index linked reference assets lost over 8% heading into April 8. Over the days leading into the April 8 S&P 500 Index low, daily net inflows for 9-15% buffer funds rose modestly from $21.7 million to $57.9 million per day with net outflows on April 4 and 7. During that same period, net inflows for 15-40% buffer products rose from $68.5 million to $147.35 million per day by April 8—topping flows across all buffer categories with no daily net outflows in between. As practitioners reacted to increasing implied volatilities and record inversion of SPX term structure3, buffer category flows demonstrated double the demand elasticity for 15-40% buffers as compared to their 9-15% buffer peers.

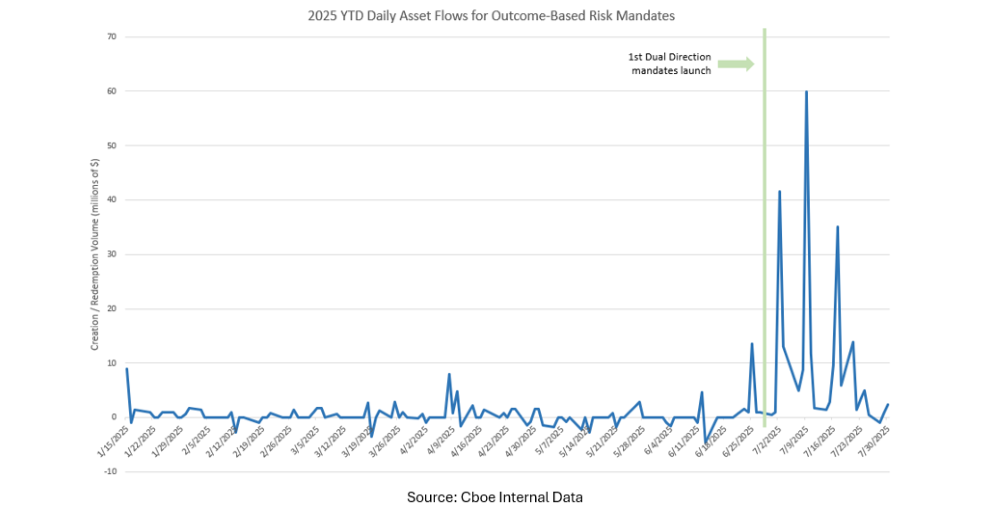

Additionally, following the April 8 S&P 500 Index inflection point, investors implemented tactical outcomes pouring nearly $15 million into “risk outcomes”4 . This outpaced Year-To-Date (YTD) flows in a nascent outcome category that makes up less than 2% of outcome-based assets5.

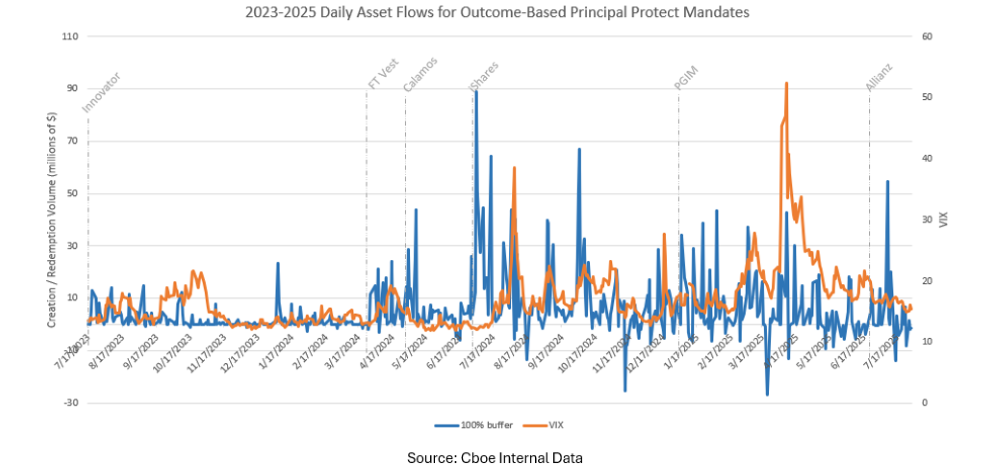

Commonly referred to as “principal protect” or “max buffer” funds, 100% buffer outcomes debuted on July 18, 2023, with the launch of the Innovator Equity Defined Protection ETF (CBOE: TJUL)—offering principal protection over a two-year outcome period. For what quickly became one of the most popular outcome-based topics of 2024, the max buffer category has burgeoned with asset flows as new entrants build out product series to meet growing investor demand.

By the end of 2024, 100% buffers topped their 9-15% and 15-40% buffer peers in terms of flows per new fund launched during the year. Category growth in 2025 remains popular as assets tied to 100% buffers have grown more than 45% YTD. Plus, new issuance shows no sign of slowing down as new and existing principal protect issuers are projected to launch three dozen new funds in 2025.6

After raising nearly $670 million in assets from January to April, flows into 100% buffers ebbed in May as investors net redeemed $9.1 million over the month. While narratives around rate and equity volatility as leading indicators of buffer flows make sense, commercial factors such as new asset managers, shorter duration outcomes and chunky, captive allocations are just as significant per the timing and magnitude of inflows. Coincidentally, max buffer flows picked up in June as geopolitical tensions in Iran and Israel increased, ending June with approximately $47 million of inflows, and more than $90 million in July so far7. Impressively, max buffer flows took second place to 9-15% buffers, while 15-40% buffers saw net outflows of $340 million over June and July.

In this still-maturing product category, new entrants continuously find ways to adapt to stiff competition by harnessing both distribution and product advantages.

We recognize some of the innovative new brands and strategies to the outcome-based category:

More than ever, outcome-based ETFs are finding utility across investors of all sophistication. With a new credit cycle on the horizon, record product innovation in outcome-based ETFs, and more managers of outcome-based solutions entering the space, Cboe is proud to be a leading listing and trading venue for outcome-based ETFs.

1 A powerful tool for a changing world | BlackRock

2 Buffer ETFs with S&P 500 exposure as reference asset

3 Since the height of the COVID crisis. Source: Cboe Macro Volatility Digest: Equity Vol Jumps the Most as Trump Tariffs Roil Markets (April 7)

4 Risk mandates are defined as potential beneficiaries of asset risk and volatility.Thus far, these mandates have included different forms of (accelerated) upside participation and income mandates.

5 As of July 15, 2025. Source: Cboe Internal Data

6 Based on 32 new launches YTD as of July 15, 2025. Compared to 39 products issued in 2024, and 1 issuance in 2023.

7 as of July 30, 2025

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/us_disclaimers/. These products are complex and are suitable only for sophisticated market participants. In certain jurisdictions, Cboe Company products are only permitted for investment professionals, certified sophisticated investors, or high net worth corporations and associations. These products involve the risk of loss, which can be substantial and, depending on the type of product, can exceed the amount of money deposited in establishing the position. Market participants should put at risk only funds that they can afford to lose without affecting their lifestyle. © 2025 Cboe Exchange, Inc. All Rights Reserved.