Read More

This Index Insights Monthly Scorecard provides an update on the performance of dozens of indices that track the levels of volatility or the performance of hypothetical strategies that invest in options or futures.

Highlights:

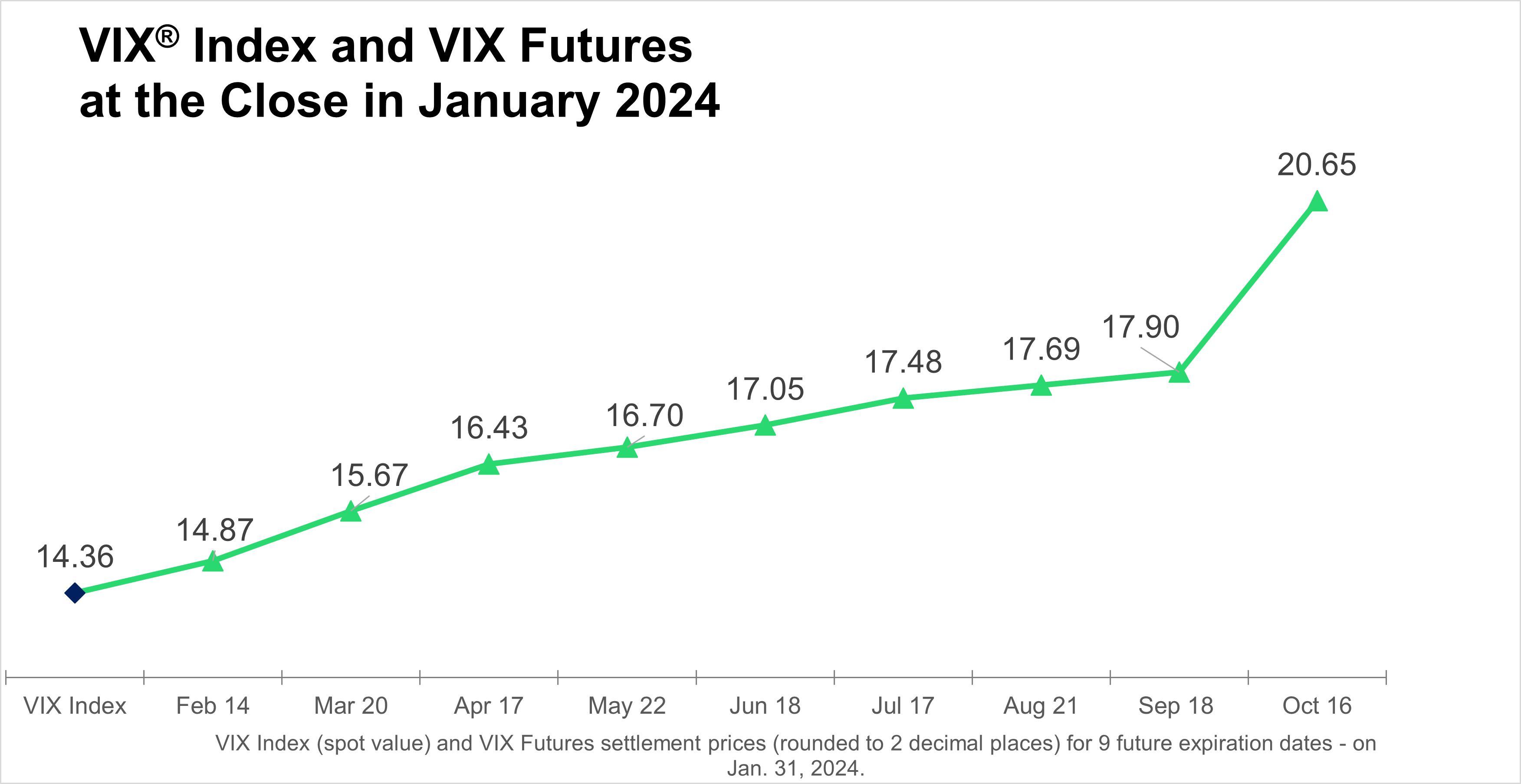

A recently published Bloomberg News article noted that traders have begun trading the newest VIX Futures contract to hedge potential U.S. election risks and highlighted that the gap between September and October VIX Futures contracts are currently wider than in 2016 and 2020.

VIX Futures were in contango on January 31 and the October VIX Futures were priced at 20.65, 15% higher than the 17.90 price for September futures.

October VIX Futures can be used as a potential hedge against potential heightened volatility around the November 5, 2024, U.S. election.

Source: Cboe Global Markets

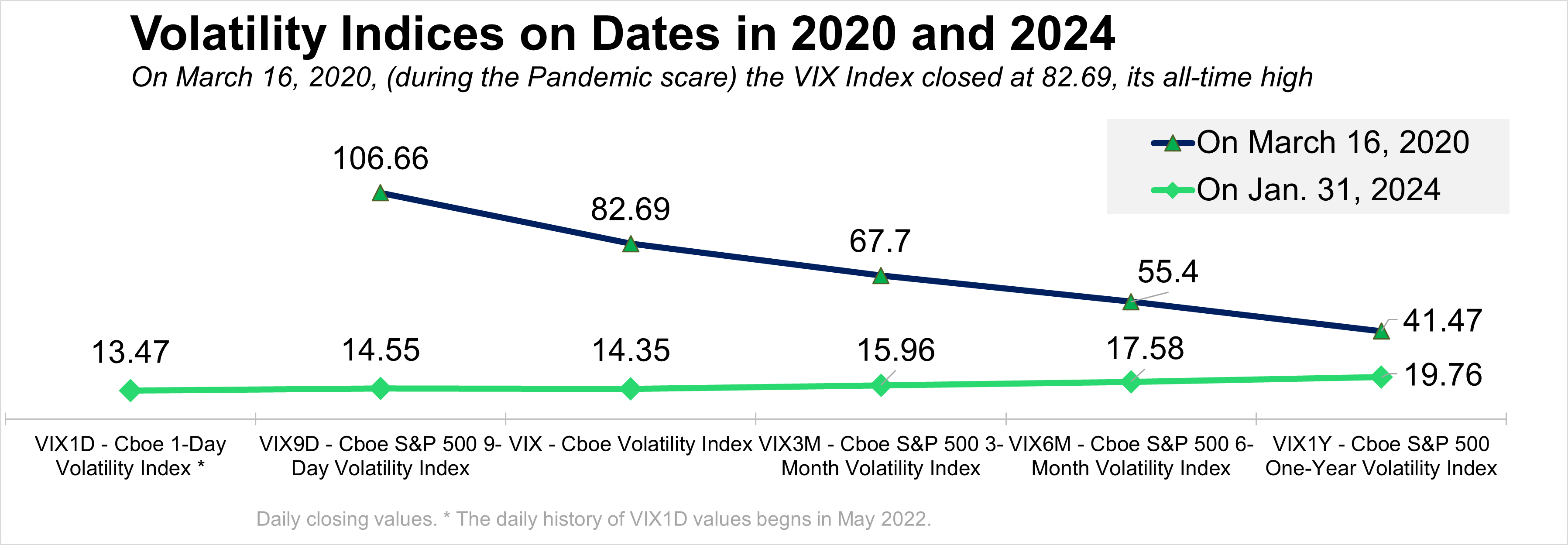

The chart below shows the term structure for S&P 500® Index options using six of Cboe’s volatility indices: VIX1DSM, VIX9DSM, VIX® Index, VIX3MSM, VIX6MSM and VIX1YSM. The VIX Index hit its all-time high daily close of 82.69 on March 16, 2020, at the start of the COVID-19 pandemic. More recently, at the end of January 2024, the VIX1Y Index reached 19.76, 12.4% higher than the 17.58 value of the VIX6M Index, reflecting investors’ expectations about the possibility of higher expected volatility in early 2025.

Source: Cboe Global Markets

Cboe offers dozens of indices that track hypothetical strategies that use index options. The table below shows the changes for three Cboe indices and three benchmarks in 2020—the last U.S. election year.

Source: Cboe Global Markets

Learn more about Portfolio Protection Using Cboe Indices, through our repository of information on index performance, white papers, webinars, option-buying strategy indices and profit-and-loss diagrams.

Interest in buffer protect strategies has grown tremendously since Cboe introduced Buffer Protect Indices in 2016.

In 2022, three of Cboe’s key Buffer Protect indices had lower losses than those of some well-known stock and bond indices.

Notably, Cboe S&P 500 15% Buffer Protect Index Balanced Series (SPRFSM) had the least severe loss at 3.7%, followed by the Cboe S&P 500 Buffer Protect Index Balanced Series (SPROSM) which fell 7.7%, and the Cboe Russell 2000 Buffer Protect Index Balanced Series (RPROSM), which fell 10.6%.

Source: Cboe Global Indices

Learn More About Buffer Protect Indices

Some of the highest five-year gains for Cboe strategy indices in the table below include:

Learn more about Cboe Global Indices and related options and futures strategies.

There are important risks associated with transacting in any of the Cboe Company products or any digital assets discussed here. Before engaging in any transactions in those products or digital assets, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/us_disclaimers/. These products and digital assets are complex and are suitable only for sophisticated market participants. These products involve the risk of loss, which can be substantial and, depending on the type of product, can exceed the amount of money deposited in establishing the position. Market participants should put at risk only funds that they can afford to lose without affecting their lifestyle. © 2024 Cboe Exchange, Inc. All Rights Reserved.